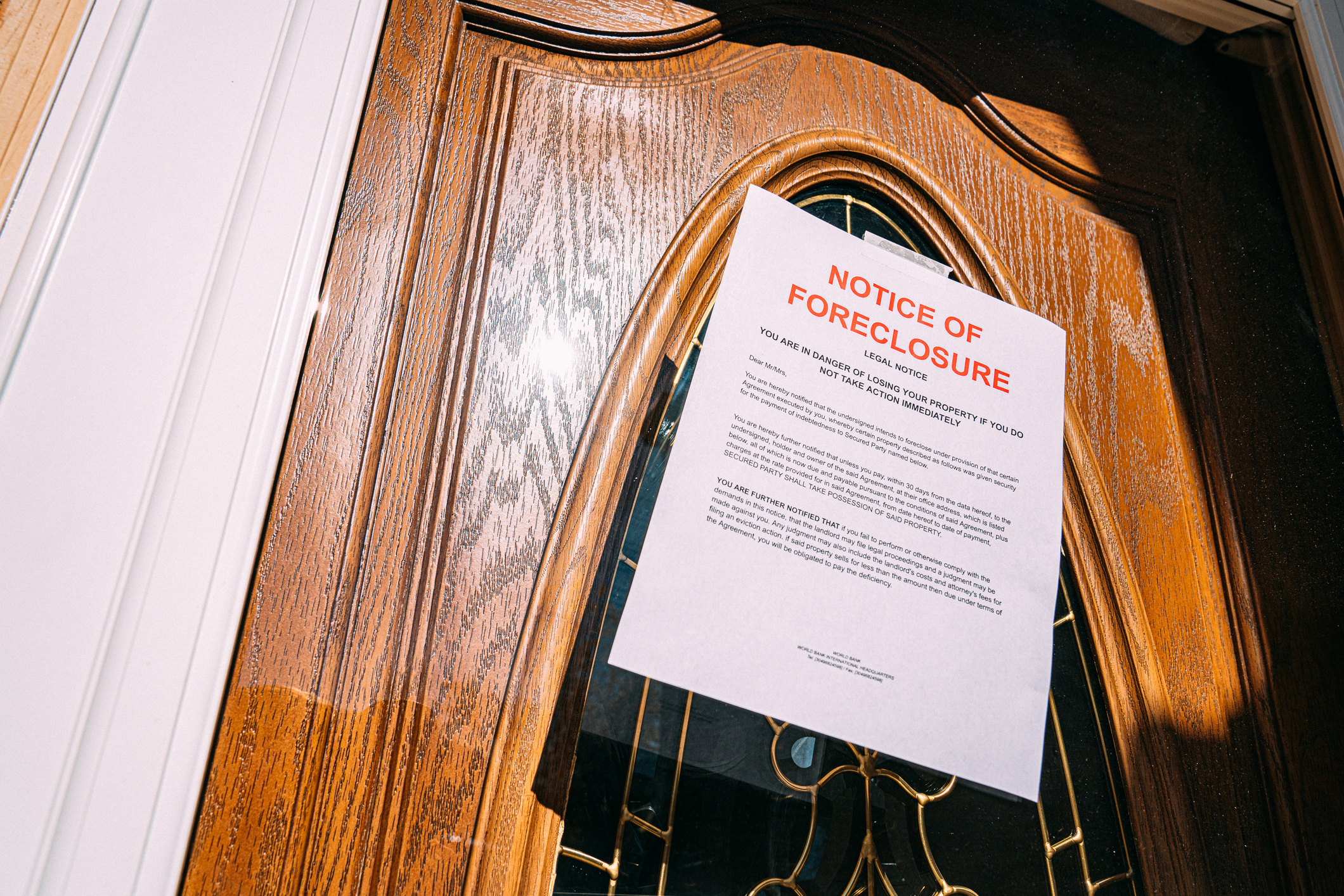

Can I Sell My House Before Foreclosure in Texas?

You can sell your house before foreclosure. You actually have the legal right to sell up until the moment the trustee conducts the foreclosure sale. So even if you’ve received a Notice of Sale or other foreclosure notice, you still have time to do something about it.

Something important to know is that Texas foreclosures are usually run under the non-judicial foreclosure system. All that means is that your lender doesn’t need to go through the court system to foreclose on your home. Instead, they use a power of sale clause in your deed of trust. This also means that the process is faster than judicial foreclosures, and you have less time to respond.

If you’re facing financial hardships and can’t keep up with your mortgage payments, definitely consider selling before foreclosure to protect your credit. Plus, it often leaves you with more money than you’d get from a short sale or deed in lieu of foreclosure. Many homeowners we’ve worked with tried loan modification or other loss mitigation options with their loan servicer without success. Maybe you’ve considered filing for bankruptcy, but want to explore other better options first. Selling to cash buyers like us might be exactly what you need to move forward.